Why High Alpha Doesn’t Always Guarantee Success

High alpha explained — why it can mislead and what other metrics matter for a full assessment.

Alpha is one of the most cited metrics in portfolio analysis. A positive number signals that a fund or ETF outperformed its benchmark after accounting for market risk — and that signal carries weight.

But alpha is often read as a verdict rather than a data point. A high figure gets treated as confirmation of quality, consistency, and repeatable skill. That assumption doesn’t always hold.

The issues are rarely visible in the number itself. They emerge when you look at what’s behind it — the time period, the portfolio structure, and the risk metrics that alpha doesn’t capture on its own.

This article explains why high alpha can be misleading, and what to look at alongside it to get a more complete picture.

Short-Term Alpha May Not Reflect the Bigger Picture

Alpha is always calculated over a specific lookback period. That window matters more than the figure it produces. A fund showing α = +4.5% over one year can show α = −0.6% over five. The asset and approach are the same, but the conclusions differ depending on the timeframe.

This isn’t a data anomaly. It reflects the reality that short periods can be dominated by a single market cycle, a sector rally, or a macro tailwind that doesn’t repeat.

Example

Consider a fund with heavy semiconductor exposure during a supply-cycle upswing.

- In the year that the sector outperforms the benchmark by 18%, the fund’s alpha looks strong.

- Twelve months later, the cycle turns — and so does the alpha.

This is why comparing alpha across multiple timeframes (1Y, 3Y, 5Y) is more informative than reading a single figure. A pattern of consistent outperformance across different market environments carries more weight than a spike in one favorable year.

Two Common Misreadings of High Alpha

High alpha isn’t always the result of broad, consistent outperformance. Two structural problems might affect how the metric is interpreted.

1. Alpha May Come from a Few Volatile Positions

A portfolio’s alpha is an aggregate figure. It doesn’t show how many positions contributed to it, or how unevenly those contributions were distributed.

In practice, a single concentrated, high-volatility holding can generate enough excess return to lift the entire portfolio’s alpha. If that position represents 15–20% of the portfolio and runs +40% in the measurement period, the overall alpha looks compelling. The problem is that this kind of alpha doesn’t reflect the strategy. It reflects a bet.

The distinction matters because concentrated alpha isn’t repeatable in the same way diversified alpha is. Once the position reverts or is reduced, the alpha goes with it. What looked like skill was largely exposure.

When evaluating alpha, it’s worth checking:

- Whether alpha is distributed across positions or driven by one or two outliers

- The tracking error — how much the portfolio deviated from its benchmark in composition, not just in return

- Whether the benchmark itself reflects the portfolio’s actual risk profile

2. Focusing on Alpha and Ignoring Beta

Alpha is calculated using beta as an input. Specifically, it measures return above what would be expected given the portfolio’s level of market sensitivity. But this creates a gap that’s easy to overlook: a high-beta portfolio, in a rising market, will systematically appear to generate alpha — even when the outperformance is simply a function of taking on more market risk.

The mechanism is straightforward:

- A portfolio with β = 1.6 and a market return of 15% has a CAPM-based expected return higher than a β = 1.0 portfolio in the same period.

- But if alpha is calculated relative to a broad index at β = 1.0, that extra performance is attributed to skill rather than market exposure.

The outperformance is real. The interpretation is not.

In a prolonged bull market, this distortion can persist for years. The same portfolio in a sustained downturn will underperform proportionally more, and its alpha will turn negative just as quickly.

High Historical Alpha Doesn’t Guarantee Future Performance

Even when alpha is real — diversified across positions, generated with controlled beta, measured over a sufficient time horizon — it doesn’t reliably predict what comes next.

Research on alpha persistence consistently shows that for most actively managed funds, performance above benchmark in one period has limited predictive value for the following period. The funds that do sustain alpha over 5–10 years represent a small minority, and distinguishing them in advance from funds that simply had a strong cycle is not straightforward.

This doesn’t make alpha useless as a metric. It makes it a starting point — not a conclusion.

How to Use Alpha Wisely

Treating alpha as one input among several, rather than a standalone signal, changes what you can reliably take from it. Here are a few concrete ways to approach it:

Check the Timeframe

Compare alpha across 1Y, 3Y, and 5Y periods before drawing any conclusions. Consistent outperformance across different market regimes is a different signal than a single strong year. If alpha looks strong over one period but flat or negative over a longer window, the short-term figure needs context.

Verify the Benchmark

Alpha is only valid when the benchmark is formally linked to the asset. A global equity fund benchmarked against the S&P 500 will produce alpha figures that don’t reflect actual performance relative to its actual asset universe. The benchmark choice is the foundation of the calculation — if it’s mismatched, the output is misleading.

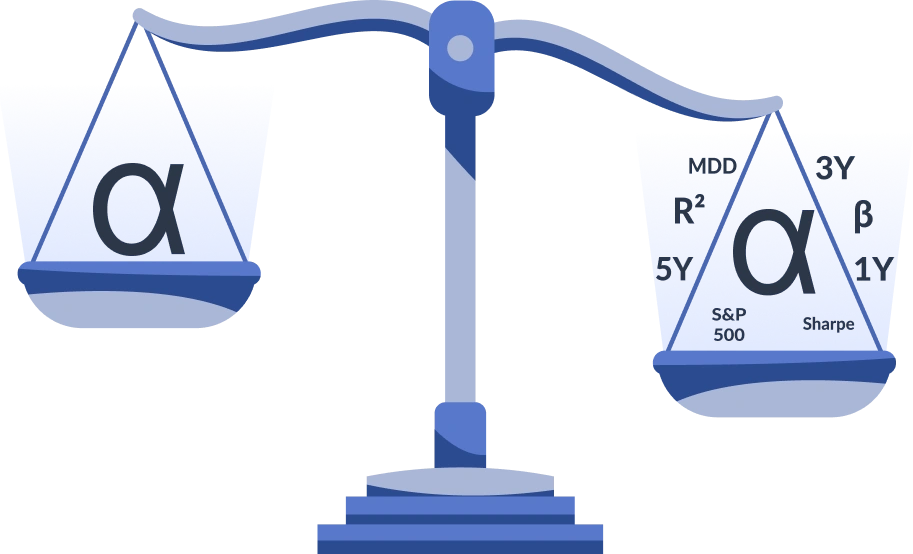

Read Alpha Alongside Beta, Sharpe, and Drawdown

These metrics answer questions that alpha doesn’t:

- Beta — how much market risk was taken to generate the result

- Sharpe ratio — risk-adjusted performance per unit of total volatility

- Maximum drawdown — the actual cost of holding the asset in adverse conditions

- R-squared — how well the benchmark explains the portfolio’s variance (low R² means the alpha is being measured against a poorly matched index)

Platforms like FinImpulse consolidate these metrics in a single view, so they can be read together rather than pulled from separate sources.

Distinguish Repeatable Alpha From Cyclical Alpha

Alpha generated through consistent factor exposure, disciplined rebalancing, or structural positioning tends to be more stable than alpha that emerged from timing a specific sector or macro trend.

One useful test: does alpha hold across different market environments, or does it concentrate in one type of market condition?

The Takeaway

High alpha is a signal worth investigating — but not one that stands on its own.

Its meaning depends on the period over which it was measured, the structure of the underlying positions, the benchmark it’s calculated against, and the beta context in which it was generated. None of that is visible in the alpha figure itself, which is precisely what makes reading it in isolation so misleading.