Why One Country Has Multiple Exchanges

An overview of why countries have multiple exchanges, how each venue fits into the broader market, and a full list of exchanges by region.

Many countries — particularly across Europe, North America, and Asia — operate not through a single exchange, but through a combination of primary listing venues, alternative trading platforms, and specialized market segments. Each of these serves a distinct function, and together they form the infrastructure through which securities are listed, priced, and traded.

This article covers how exchanges are structured across major markets, why multiple venues coexist within a single country, and what that layered architecture means for anyone working with cross-market financial data.

Exchange: Definition and Core Functions

An exchange is a regulated marketplace where financial instruments are listed and traded. Depending on the venue, those instruments may include equities, bonds, derivatives, commodities, or ETFs.

Core functions across all exchange types are:

- Listing — providing a structured, regulated environment for issuers to make their instruments publicly tradable

- Price discovery — continuous order matching that reflects supply and demand in real time

- Liquidity provision — ensuring sufficient market depth for buyers and sellers to transact

Exchanges also set and enforce listing requirements: minimum capitalization thresholds, disclosure standards, corporate governance rules, and ongoing reporting obligations. The strictness of these requirements varies significantly between venues, and that variation is one of the structural reasons multiple exchanges operate within the same market.

Structural Drivers of Exchange Fragmentation

There are four main reasons why a country may have more than one exchange:

Historical Decentralization

Before the advent of electronic trading, financial activity was geographically dispersed. In countries with strong regional economies, major cities developed their own exchanges independently.

Germany is the clearest example: Berlin, Frankfurt, Munich, Stuttgart, Hamburg, Hanover, and Düsseldorf all have established exchanges that reflect their local commercial centers.

Electronic trading consolidated volume onto national platforms, but the organizational structures of regional exchanges largely remained.

Market Segmentation by Company Profile

Different exchanges serve different types of issuers. A single country may operate a main market for large, established companies alongside a separate venue — with lower listing thresholds and lighter regulatory requirements — for smaller or early-stage businesses.

This segmentation allows regulators and market operators to apply appropriate oversight without imposing the full compliance burden of a premium listing on companies that don’t yet meet those criteria.

Competition for Order Flow

Alternative trading venues exist not to host new listings, but to compete with primary exchanges on execution. Multilateral Trading Facilities (MTFs) attract order flow by offering narrower spreads, faster execution, or lower transaction costs.

From a market structure perspective, this competition is generally considered beneficial — it keeps pricing efficient and reduces costs for institutional traders. The result, however, is that liquidity for a given security is often distributed across several venues simultaneously.

Technical Separation of Listing and Trading Infrastructure

As markets modernized, the functions of an exchange — listing, regulation, and trade execution — were sometimes separated into distinct systems. An exchange can operate its own electronic trading engine while maintaining its identity as a separate regulatory organization.

This distinction is consequential for data: records from the “exchange” and records from its “trading engine” can appear as separate venues in a market data feed.

Real-Market Examples

The UK and Germany illustrate how the structural factors described above play out in real markets. Both are major financial centers — but their exchange landscapes developed differently, and understanding each one clarifies what a multi-venue structure actually looks like in practice.

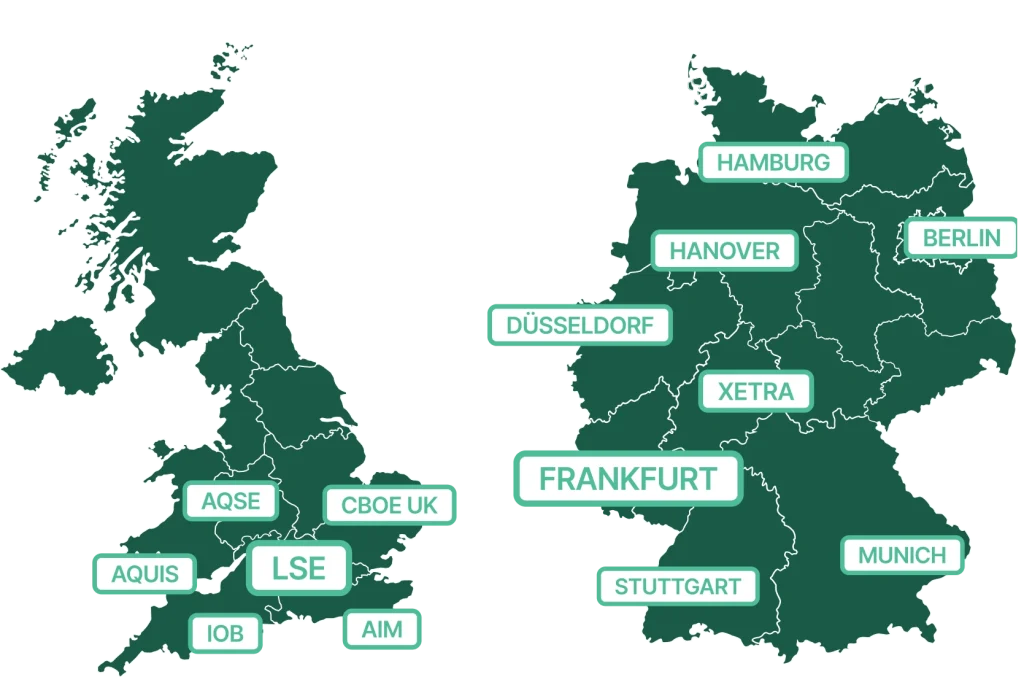

The United Kingdom: Layered Market Structure

The UK market is organized across several distinct venues, each occupying a specific role in the broader ecosystem.

- London Stock Exchange (LSE) — the primary national exchange. It operates two main listing categories: the Premium segment, which applies the most stringent standards and is the default venue for FTSE 100 constituents, and the Standard segment, which applies EU minimum standards and is more accessible to international issuers.

- AIM (Alternative Investment Market) — a sub-market of the LSE, launched in 1995 specifically for smaller and growth-stage companies. It operates under a lighter regulatory framework — companies are overseen by a nominated advisor (Nomad) rather than directly by the Financial Conduct Authority (FCA) for listing purposes. AIM has become one of the most active growth markets in Europe, with over 700 companies listed.

- Aquis AQSE (Aquis Stock Exchange) — an independent exchange that competes with AIM for smaller listings. It operates its own recognition as a Recognised Investment Exchange (RIE) and offers an alternative for early-stage companies that prefer its fee structure or market model.

- Cboe UK — not a listing exchange. It is an MTF that trades securities already listed on the LSE and other venues. Its role is execution: it competes for order flow by offering pricing and speed advantages to institutional and algorithmic traders.

- IOB (International Order Book) — a segment within the LSE designed for international equities, primarily accessed through Global Depositary Receipts (GDRs). It functions as a gateway for non-UK companies to access UK-based capital markets without a full domestic listing.

Overall, the UK operates as a multi-venue market where listing and trading are separate layers.

Germany: Regional History and Electronic Consolidation

Germany’s exchange structure reflects its federal history. Unlike markets that developed around a single financial capital, Germany’s financial system was built across multiple regional centers — each with its own exchange.

Frankfurt Stock Exchange and XETRA

The Frankfurt Stock Exchange is Germany’s primary listing venue and the country’s largest exchange by market capitalization. However, the majority of equity trading does not occur on Frankfurt’s regulated market — it takes place on XETRA, an electronic trading platform operated by Deutsche Börse Group.

These are not interchangeable terms:

| Frankfurt Stock Exchange | XETRA | |

|---|---|---|

| Type | Regulated exchange (listing venue) | Electronic trading platform |

| Function | Listing, regulatory oversight | Order matching, trade execution |

| Volume | Minority of German equity trades | ~90% of German equity volume |

| Operator | Deutsche Börse AG | Deutsche Börse AG |

In a market data context, Frankfurt and XETRA appear as separate venues. Price data sourced from XETRA represents the dominant liquidity pool for German equities, while Frankfurt floor data is comparatively thin.

Regional Exchanges

Germany’s six regional exchanges — Berlin, Munich, Stuttgart, Hamburg, Hanover, and Düsseldorf — operate as formally recognized venues. Each maintains its own order book and can show marginally different prices for the same instrument at any given moment, depending on local supply and demand.

In practice, their role has narrowed considerably. Stuttgart (Börse Stuttgart) is the most active among them, with a strong focus on retail trading in bonds, structured products, and ETFs — a niche not fully served by XETRA. The others primarily serve domestic retail investors and regional brokerage flow.

What This Means for Market Data

All of these have direct consequences for market data: venue and country are not interchangeable. The same instrument can trade across several venues simultaneously, with liquidity distributed between them.

Without an exchange identifier, data for a given ticker is ambiguous, as it may come from the primary listing exchange, an MTF, or a regional platform with considerably thinner order flow. This is why venue-level identifiers matter.

In FinImpulse, every ticker displays the exchange it trades on — visible in the header of each ticker page in the FinImpulse dashboard.

The same identifier is available in the FinImpulse API as the “exchange” field.

This enables filtering by specific venue, aggregating by country, or programmatically distinguishing primary listing data from execution venue data.

Global Exchange Coverage by Region

Below is a full list of exchanges covered across all major regions — from primary national venues to alternative platforms and specialist facilities.

| Region | Country | Exchanges |

|---|---|---|

| North America | United States | Nasdaq, Nasdaq GIDS, NasdaqCM, NasdaqGM, NasdaqGS, NYSE, NYSE American, NYSE Arca, Cboe US, Chicago Options, OTC Markets EXMKT, OTC Markets Grey, OTC Markets OTCPK, OTC Markets OTCQB, OTC Markets OTCQX |

| Canada | Toronto, TSXV, Canadian Sec, Cboe CA | |

| Mexico | Mexico | |

| Europe | United Kingdom | LSE, AIM, Aquis AQSE, Cboe UK, IOB |

| Germany | Frankfurt, XETRA, Berlin, Munich, Stuttgart, Düsseldorf, Hamburg, Hanover | |

| France | Paris | |

| Netherlands | Amsterdam | |

| Belgium | Brussels | |

| Portugal | Lisbon | |

| Spain | MCE | |

| Italy | Milan | |

| Switzerland | Swiss Exchange | |

| Austria | Vienna | |

| Ireland | Irish Stock Exchange | |

| Denmark | Copenhagen | |

| Finland | Helsinki | |

| Norway | Oslo | |

| Sweden | Stockholm | |

| Iceland | Nasdaq Iceland | |

| Poland | Warsaw | |

| Czech Republic | Prague | |

| Hungary | Budapest | |

| Romania | BVB | |

| Baltics | Riga (Latvia), Tallinn (Estonia), Vilnius (Lithuania) | |

| Pan-European | Euronext, Cboe Europe | |

| Asia | China | Shanghai, Shenzhen |

| Hong Kong | HKEX | |

| Japan | Tokyo, Sapporo, Fukuoka | |

| South Korea | KSE, KOSDAQ | |

| India | NSE, BSE, MCX | |

| Taiwan | TWSE, Taipei Exchange | |

| Vietnam | HOSE | |

| Thailand | SET | |

| Indonesia | Jakarta | |

| Malaysia | Kuala Lumpur | |

| Pakistan | Karachi | |

| Sri Lanka | Colombo | |

| Middle East | UAE | Dubai |

| Qatar | Qatar | |

| Kuwait | Kuwait | |

| Saudi Arabia | Saudi Exchange (Tadawul) | |

| Israel | Tel Aviv | |

| Turkey | Borsa Istanbul | |

| Africa | South Africa | Johannesburg |

| Egypt | EGX | |

| Latin America | Argentina | Buenos Aires |

| Brazil | São Paulo (B3) | |

| Chile | Santiago | |

| Venezuela | Caracas | |

| Colombia | BVC | |

| Oceania | Australia | ASX, Cboe AU |

| New Zealand | NZX | |

| Other/Specialized | — | NAE, Singapore Exchange (SES), TLO, YHD |

The Takeaway

Most markets operate through a combination of listing venues, alternative platforms, and regional exchanges — each with a distinct role and a distinct data footprint.

Knowing which venue a record comes from is the detail that makes data usable — and it is part of how FinImpulse structures its data.